Haven't joined yet? Get 20% OFF now on your first purchase! Use code

Claim Discount· LIMITED TIME OFFERFinding a crypto prop firm with free market data and reliable real time pricing is more important than many traders think. Access to clean market data shapes execution quality, pricing accuracy, and overall trading performance. Today, more traders are focusing on firms that provide true free market data instead of delayed or synthetic feeds, making data quality a key factor in choosing the right prop firm.

Free market data in crypto prop trading refers to real time exchange information, such as price feeds, order book depth, trading volume, and historical candles, provided by a prop firm without additional fees. It allows traders to see accurate market conditions similar to major exchanges, instead of delayed or synthetic pricing models.

For a broader understanding of how these systems operate across different platforms, see crypto prop firms overview.

In practice, free market data determines how precisely trades are executed, how reliably price movements are reflected on charts, and how effectively strategies can be tested and applied. Prop firms that provide true free market data aim to mirror real exchange environments, giving traders access to transparent and up to date market conditions.

Real time exchange data comes directly from live market activity, reflecting actual buy and sell orders as they happen. In contrast, synthetic pricing models generate artificial or delayed prices that may not fully match real exchange conditions, leading to less accurate trading insights.

Not all free market data offered by prop firms is equal. Some firms provide true real time exchange feeds, while others use delayed, filtered, or simulated data. The quality of the data directly depends on the firm’s infrastructure and connection to actual exchange liquidity.

Market data in crypto trading is built from several key components that define its accuracy and usefulness:

Market data quality is one of the most critical factors in crypto prop trading because it directly influences how accurately trades are executed, how prices are interpreted, and how strategies perform under real market conditions. Even a strong trading strategy can underperform if the underlying market data is delayed, incomplete, or inconsistent with real exchange conditions. High quality market data ensures traders are making decisions based on accurate, real time information that reflects true market liquidity and price movement.

Execution accuracy depends heavily on how fast and precisely market data is delivered. In crypto prop trading, even small delays in price updates can cause entries and exits to occur at unintended levels. Real time, high quality market data ensures that chart prices closely match actual exchange prices, allowing traders to time entries more effectively and reduce discrepancies between expected and executed trades. This becomes especially important for short term strategies where timing is a key edge.

Slippage and Hidden Trading Costs

Poor quality or delayed market data often leads to execution mismatches, where trades are filled at prices different from what the trader sees on the chart. These differences create hidden costs that gradually erode profitability, especially in fast moving markets. When market data is not aligned with real exchange conditions, traders may experience inconsistent fills, making it harder to manage risk and maintain predictable performance over time.

Strategy Performance in Volatile Markets

During periods of high volatility, market data quality becomes even more important. Rapid price movements require instant and accurate updates to reflect true market conditions. If data is delayed or simplified, strategies such as breakout trading, scalping, or liquidity based setups may generate false signals or unreliable entries. High quality market data allows traders to evaluate volatility correctly, adapt strategies in real time, and maintain consistency even in fast changing market environments

Crypto prop firms use different types of market data systems depending on their infrastructure, cost structure, and execution model. These systems range from simplified synthetic pricing to advanced direct liquidity connections. The type of market data a firm uses has a direct impact on price accuracy, execution quality, and overall trading experience.

Synthetic CFD based models generate prices internally rather than pulling directly from real exchange order books. These systems simulate market movements using reference data or internal algorithms. While they can appear stable on charts, they often do not fully reflect real market depth or true liquidity conditions, which can create differences between displayed prices and actual exchange behavior.

Aggregated exchange feeds combine data from multiple liquidity providers or exchanges into a single unified price stream. This approach improves price coverage and reduces reliance on a single source, but it may still introduce slight delays or inconsistencies in order book depth. Traders using this type of data typically receive a more balanced view of the market, but not always full real time granularity.

Direct exchange API feeds pull market data straight from a single exchange such as Binance or Bybit. This method provides more accurate and timely information compared to aggregated or synthetic models. It includes real time price updates, partial or full order book data, and live volume metrics, making it suitable for more advanced trading environments that require closer alignment with actual market conditions.

Direct liquidity execution models represent the most advanced form of market data integration. In this system, pricing and execution are closely tied to real exchange liquidity pools, aiming to replicate actual market conditions as closely as possible. This model reduces discrepancies between displayed and executed prices and is designed for traders who require institutional grade accuracy and responsiveness in fast moving markets.

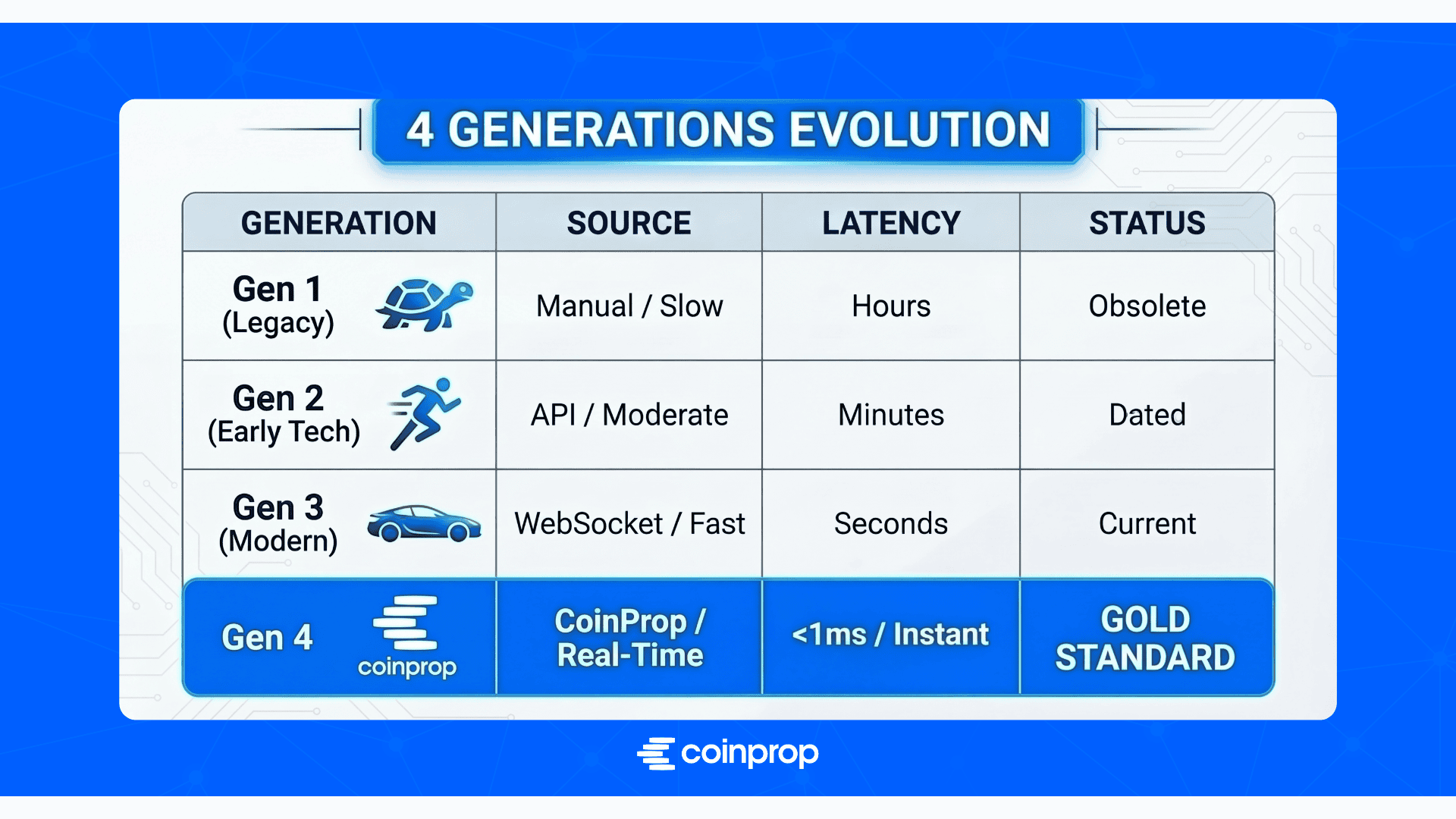

The evolution of market data systems in crypto prop firms reflects the industry’s shift from simulated pricing environments to near institutional execution standards. Each generation represents improvements in speed, transparency, and alignment with real exchange conditions. Understanding this progression helps traders evaluate how closely a prop firm replicates actual market behavior.

Gen 1 systems rely on synthetic or internally generated price feeds rather than real exchange order books. These prices are often simulated using simplified models, which can lead to mismatches between displayed charts and actual market conditions. As a result, execution accuracy and price transparency are limited compared to real exchange environments.

Gen 2 systems improve on synthetic pricing by combining data from multiple sources, such as liquidity providers and exchange feeds. This creates a more stable pricing environment, but it may still include delays or incomplete order book representation. While more reliable than Gen 1, it does not fully replicate real time exchange depth.

Gen 3 systems connect directly to exchange APIs, providing real time market data including price updates, partial or full order book information, and live volume data. This model is widely considered the current industry standard because it closely reflects actual exchange conditions while maintaining stable infrastructure for prop trading environments.

Gen 4 systems represent the most advanced market data and execution model, where pricing and order execution are closely aligned with real exchange liquidity pools. This setup minimizes discrepancies between displayed and executed prices and is designed to replicate institutional level trading conditions. It offers the highest level of realism in crypto prop trading environments.

Identifying whether a crypto prop firm provides real market data is essential for evaluating execution quality and trading reliability. Traders should focus on measurable technical indicators such as order book depth, latency performance, and price consistency with major exchanges. A firm that offers true real market data will closely mirror actual exchange conditions, ensuring transparent and accurate trading environments.

A legitimate market data system provides visible and meaningful order book depth, showing real liquidity levels at multiple price points. Transparent order book data allows traders to assess market pressure, identify liquidity zones, and evaluate how realistic the trading environment is. Limited or shallow order book information may indicate reduced data quality or simulated pricing structures.

Latency is a key indicator of market data quality. Professional grade systems typically operate with sub 100ms latency, ensuring near real time updates that reflect live market conditions. In contrast, delayed feeds introduce noticeable gaps between actual exchange prices and displayed data, which can affect execution timing and reduce trading precision.

One of the most reliable ways to verify real market data is by comparing a prop firm’s prices with major exchanges such as Bybit and Binance. If price movements, candles, and spread behavior consistently match in real time, it indicates a direct or high quality data feed. Significant discrepancies or delays may suggest synthetic or aggregated pricing models instead of true exchange level data.

Fake or low quality market data systems often show warning signs such as inconsistent pricing compared to major exchanges, missing or shallow order book information, and delayed chart updates during high volatility. Another red flag is overly smooth price movement that does not reflect natural market fluctuations. These indicators suggest that the data may be simulated or heavily filtered rather than sourced from real exchange activity.

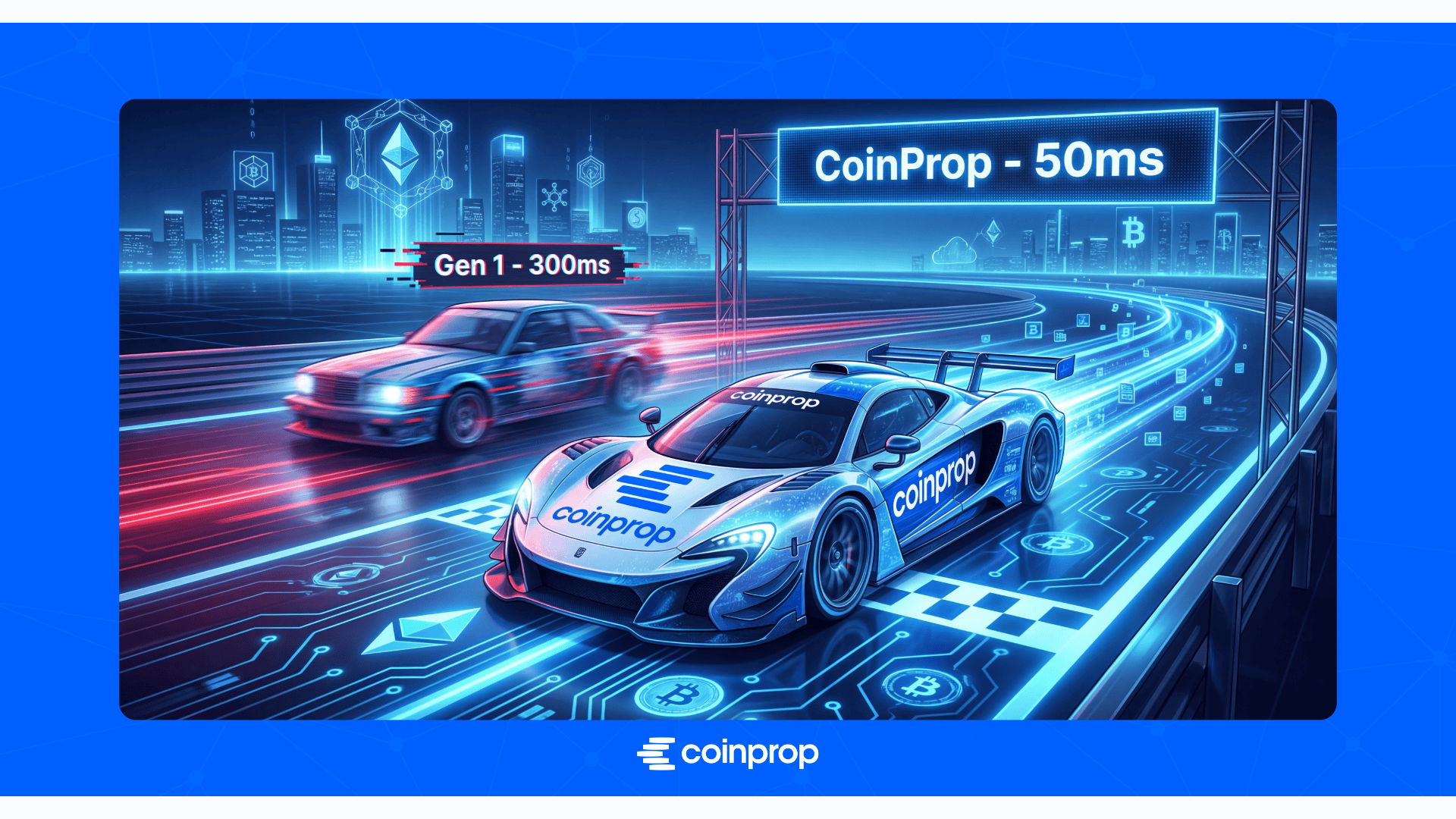

Gen 1 and Gen 2 market data models are gradually being phased out in modern crypto prop trading because they fail to meet the increasing demand for real time accuracy, transparency, and institutional level execution quality. As traders become more sophisticated and markets move faster, these older systems struggle to replicate true exchange conditions, making them less suitable for serious trading environments.

One of the main weaknesses of Gen 1 and Gen 2 systems is poor execution accuracy during periods of high market volatility. Because these models often rely on synthetic or aggregated data, price updates may not fully reflect rapid market movements. This can result in execution mismatches where trades are filled at significantly different levels than expected, reducing consistency and making performance less predictable in fast moving conditions.

Gen 1 and Gen 2 models typically provide limited or no access to a full, real time order book. Without deep visibility into market liquidity, traders cannot accurately assess buy and sell pressure or identify key liquidity zones. This lack of transparency reduces the ability to make informed trading decisions, especially for strategies that rely heavily on order flow analysis and liquidity dynamics.

Modern crypto traders increasingly expect execution quality that closely mirrors real exchange environments. This has driven demand for systems that offer direct exchange level data, full order book transparency, and low latency updates. As a result, Gen 1 and Gen 2 models are being replaced by more advanced infrastructure that better supports professional trading strategies and institutional style execution standards.

CoinProp’s market data infrastructure is designed around providing real time, exchange aligned pricing and execution conditions through a direct market data approach. The goal of this system is to reduce discrepancies between displayed prices and actual market conditions, allowing traders to operate in an environment that closely resembles live exchange trading. By focusing on data accuracy and speed, the infrastructure aims to support more consistent decision making and execution reliability.

The direct market data architecture is built to deliver real time price updates sourced from high quality exchange connections. Instead of relying on heavily filtered or synthetic pricing layers, the system prioritizes a more direct flow of market information, including price movements, liquidity signals, and order book behavior. This structure is designed to improve transparency and ensure that traders are working with data that closely reflects real market conditions.

Execution speed plays a critical role in how effectively market data is translated into real trades. A low latency infrastructure helps ensure that price updates and order execution happen with minimal delay, reducing the gap between market movement and trade action. This level of responsiveness is especially important in fast moving crypto markets where small timing differences can significantly impact trade outcomes.

A key objective of this infrastructure is to replicate the behavior of major crypto exchanges as closely as possible. This includes aligning price movements, order book behavior, and execution flow with real market dynamics. By mirroring these conditions, traders experience a more realistic trading environment that better reflects how strategies would perform on actual exchanges.

When market data is consistent and closely aligned with real exchange conditions, trading strategies tend to perform more predictably. Accurate data helps reduce unexpected deviations in entries and exits, allowing for better risk management and more stable execution patterns. This consistency is especially important for traders relying on systematic strategies, where small data inconsistencies can compound into larger performance differences over time.

In crypto prop trading, there is often a noticeable gap between marketing claims and actual execution quality. Many prop firms advertise free market data or real time pricing, but the underlying infrastructure can vary significantly. Understanding this gap is important because trading results depend far more on execution quality and data integrity than on strategy alone.

Many prop firms promote free market data as a key advantage, but the reality behind these claims can differ. Some firms provide true real time exchange aligned feeds, while others rely on aggregated or partially simulated pricing systems. While both may appear similar on charts, the execution experience can vary, especially when orders are placed in fast moving market conditions. This difference between marketing language and actual data quality is often not immediately visible to traders.

Even small delays in market data updates can have a noticeable impact on trade execution. When price feeds are not fully synchronized with real exchange conditions, traders may see entry and exit prices that differ from actual fills. Over time, these small inconsistencies can affect overall performance, especially for strategies that depend on precision and timing. Hidden delays are often subtle but can accumulate into meaningful differences in trading outcomes.

Many traders struggle not because their strategies are weak, but because the execution environment does not fully reflect real market conditions. When market data is delayed, incomplete, or inconsistent, even well tested strategies can produce unexpected results. This mismatch between strategy design and execution reality is one of the most common reasons traders fail in prop firm challenges or underperform in live trading environments.

Choosing a crypto prop firm should not be based on marketing claims or leverage offers alone. The most important factor is the quality of the trading infrastructure, especially market data accuracy and execution reliability. Traders who evaluate firms based on technical conditions rather than surface level features are more likely to find environments that support consistent performance and realistic trading outcomes.

A serious prop trading infrastructure should provide stable, real time market data, consistent execution, and transparent pricing behavior. At a minimum, traders should expect accurate price feeds that reflect live market conditions, responsive order execution, and a system that does not significantly deviate from major exchange pricing. Without these fundamentals, even advanced strategies can become unreliable in practice.

Evaluating market data quality requires checking several key elements. A reliable prop firm should offer visible order book depth that reflects real liquidity, low latency price updates that closely match exchange movements, and pricing consistency with major platforms. When these elements are aligned, traders can trust that the environment reflects actual market behavior rather than simulated or delayed data.

While leverage is often highlighted as a key selling point, the execution environment has a far greater impact on long term trading performance. High leverage without accurate market data can increase risk exposure without improving execution quality. In contrast, a realistic trading environment with high quality data allows traders to manage risk more effectively and execute strategies with greater precision, which ultimately matters more than leverage levels alone.

In crypto prop trading, the biggest advantage rarely comes from strategy alone. It comes from the quality of market data and the accuracy of execution. As prop firm models continue to evolve, traders who prioritize real time, exchange aligned data over marketing claims tend to experience more consistent and predictable results. Ultimately, market data quality is what determines how closely a trading environment reflects real market conditions.

Across different prop firm systems, market data can range from synthetic and delayed feeds to direct exchange level connections. Lower tier models often rely on simulated or aggregated pricing, which can reduce transparency and execution accuracy. Higher tier systems focus on real time exchange integration and deeper liquidity visibility, providing a more realistic trading experience. These differences directly affect how strategies perform in live conditions.

In modern crypto markets, execution quality often has a greater impact on results than strategy design. Even well developed strategies can underperform if market data is delayed or inconsistent with real exchange conditions. Accurate, low latency data ensures that entries, exits, and risk management decisions reflect actual market behavior, making execution a more critical factor than theoretical strategy advantages.

For prop traders, the key takeaway is simple: focus on infrastructure before leverage or promotions. A prop firm with high quality market data provides a more reliable environment for testing, refining, and executing strategies. By prioritizing execution quality and data integrity, traders can build more consistent performance and reduce the gap between backtesting results and real trading outcomes.

This section answers the most common questions traders have about free market data in crypto prop firms, including how it works, how to evaluate its quality, and why it matters for trading performance.

In many prop firms, free market data means that traders are not charged separately for accessing live pricing feeds. However, the actual quality of that data can vary. Some firms provide real time exchange aligned data as part of their infrastructure, while others may use delayed or aggregated feeds while still marketing them as free. The key difference is not the price, but the accuracy and source of the data.

Professional grade market data typically operates with very low latency, often under 100 milliseconds. At this level, price updates closely reflect real time exchange movements, allowing for more accurate execution and timing. Higher latency systems can introduce delays between actual market changes and displayed prices, which may reduce precision in fast moving trading conditions.

Yes, market data quality can significantly influence challenge outcomes. When traders receive accurate and real time pricing, their entries, exits, and risk management decisions are more aligned with actual market conditions. In contrast, delayed or inconsistent data can distort trade execution and make it harder to replicate expected strategy performance during evaluation phases.

Traders can verify market data quality by comparing price movements with major exchanges in real time, checking order book depth, and observing execution consistency during volatile periods. If a prop firm’s prices closely match exchanges like Binance or Bybit and reflect real time liquidity behavior, it is more likely to be using genuine exchange linked data rather than synthetic pricing models.

Before choosing a funded account, it's worth understanding how a crypto prop firm manages risk, evaluates performance, and handles payouts.